Should You Sell Dubai Real Estate Amidst the Iran Crisis? Short-Term Impacts and Future Outlook Based on Past Precedents

As of March 2026, concerns are growing that the tightening situation in the Middle East might lead to a significant collapse of Dubai's real estate market. Indeed, it cannot be denied that in phases where regional tensions worsen, new prospective buyers may adopt a wait-and-see approach, potentially leading to a short-term slowdown in transactions.

However, looking back at past crisis periods in the Dubai real estate market, it hasn't completely collapsed with every external shock. Instead, it has a history of recovery driven by institutional improvements, capital inflows, and a return of demand.

It is crucial to distinguish between immediate anxieties and structural declines.

This article will clarify current concerns surrounding the potential Iran conflict, and then review past cases such as the 2008 Dubai Shock, the adjustment phase from 2014 to 2019, COVID-19, and the 2024 floods, to outline how we should view the current Dubai real estate market.

In conclusion, the baseline scenario is "short-term stagnation," not a "complete collapse"

When considering the current geopolitical risks, the first thing to bear in mind is that sensational news headlines do not always align with market realities. When the situation deteriorates, those considering purchases involving on-site visits or short-term trading tend to become cautious. As a result, it is quite possible for the number of inquiries, viewings, and contract speeds to temporarily slow down.

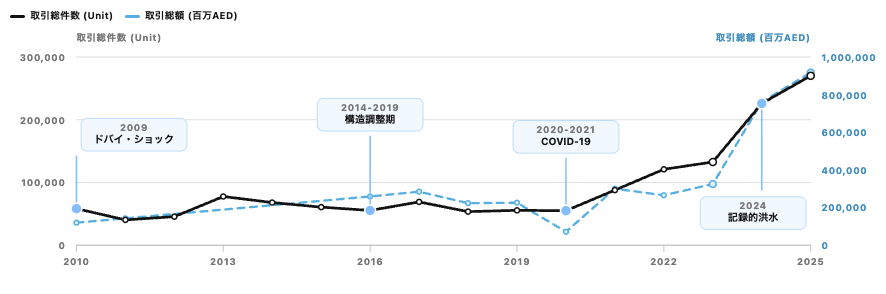

On the other hand, looking at trends over the past 20+ years, the Dubai market has not seen demand drop to zero during crises; instead, it has recovered after temporary stagnation. Transaction volumes since 2010 have continued to set new records, even as they plateaued during crisis periods. According to available data, total transaction volumes have expanded from 58,293 units in 2010 to 226,000 units in 2024, and an estimated 270,000 units in 2025. The market's depth itself has clearly increased compared to past crises.

Therefore, what should be watched out for at present is not a sudden price collapse, but rather a slowdown in transactions due to short-term sentiment deterioration. Regarding prices, even if an adjustment occurs, it is likely to be differentiated by property grade and area, rather than a uniform market-wide decline.

Why a 2008-style collapse is unlikely

When considering the downside risks for the Dubai real estate market, many people immediately recall the Dubai Shock of 2008-2009. At that time, the global financial crisis combined with excessive leverage, plunging the market into severe turmoil. Prices are said to have fallen by approximately 50% to 60% from their peak, and recovery took a long time.

However, the market structure is significantly different between then and now. The market around 2008 was highly vulnerable due to speculative capital and a high reliance on borrowing. Since then, Dubai has seen the strengthening of RERA's functions, the establishment of an escrow system, and the introduction of LTV regulations, making it a much more regulated market than it was then.

In other words, for a severe systemic instability like that of 2008 to recur, a mere increase in geopolitical risk is insufficient. It would require a simultaneous destabilization of the financial system and a chain of excessive borrowing. The current concerns are primarily related to sentiment and regional security, making it difficult to equate them with a 2008-style market collapse, which is the fundamental view.

The "self-adjusting capability" shown in the 2014-2019 adjustment phase

Next, the structural adjustment phase from 2014 to 2019 offers a valuable reference. During this period, a combination of low oil prices, increased supply, and a strong dollar exerted downward pressure on the market. Prices adjusted gradually over several years but did not lead to a crash like in 2008.

What was confirmed during this phase was the Dubai market's self-adjusting capability. When prices fell, real demand previously out of reach entered the market, and transactions continued. As a result, the market matured to include a broader range of buyers, not just ultra-high-net-worth individuals.

This experience is crucial in situations where external shocks are anticipated, such as the current one. Even if some prices weaken due to a short-term deterioration in sentiment, it does not necessarily translate immediately into overall market dysfunction. There remains ample room for transactions to continue through supply and demand adjustments.

During COVID-19, a V-shaped recovery occurred after a standstill

The 2020 pandemic was an extremely severe shock for the real estate market, as it involved physical movement restrictions. Immediately after the lockdown, transactions stagnated, and prices weakened. However, the subsequent recovery was remarkably swift, and the Dubai market entered a major upward phase from 2021 onwards.

The underlying reason was that Dubai had become a city chosen not just as an investment destination, but also as a place of residence, a business hub, and a safe haven for asset preservation. Early economic reopening, expansion of visa schemes, and an influx of international talent and high-net-worth individuals propelled the recovery. This phase demonstrated that even if pessimism intensifies immediately after a crisis, demand can return as long as Dubai's urban competitiveness itself is not lost.

Concerns regarding the current potential Iran conflict must also be viewed from the same perspective. While a short-term slowdown in transactions is possible, Dubai's structural role as a magnet for regional capital and talent will not be immediately lost. In fact, instability in neighboring countries could even generate demand for refuge or diversification towards Dubai.

Even with the 2024 floods, the market did not significantly collapse

The record floods in April 2024 presented another type of stress test for Dubai's real estate market. Some areas indeed experienced flooding, intensifying concerns that prices might collapse due to flood risk.

However, subsequent data confirmed the market's resilience. In May 2024, the month after the floods, residential property prices continued to rise month-on-month, and transaction volumes remained high. Crucially, major developers quickly responded with repairs, and the government announced plans to strengthen drainage infrastructure. In Dubai, when issues arise, there's a functional structure in place where trust is maintained through policy responses and developer actions, rather than problems being left unaddressed.

This point is also important when assessing geopolitical risks. Market participants are not just looking at the shock itself. How the government, developers, and financial institutions respond to the shock directly impacts the preservation of prices and demand.

Short-term impacts to anticipate from the current potential Iran conflict

What is most likely to happen in the current situation is a temporary delay in buyers' decision-making. Especially overseas investors who are not in a hurry to make investment decisions, and those considering purchases based on on-site visits, tend to postpone contracts until the situation stabilizes. Therefore, in the short term, the lead time from inquiry to contract may lengthen, and transaction volumes could decelerate.

Furthermore, the impact will not be uniform across all segments. Mid-price segments and those focused on investment yield are more susceptible to sentiment and likely to experience price negotiations. Conversely, rare waterfront properties and ultra-luxury segments may be relatively more resilient. This is because such assets are sometimes seen as 'safe havens' during times of crisis.

Moreover, sellers' reactions will also vary. Owners with low leverage will not need to rush sales and can more easily protect prices, whereas those aiming for short-term resale may increase profit-taking or early sales. Future price trends will also be influenced by these differences in seller composition.

Mid-term scenario: "Crises can attract demand"

A characteristic of the Dubai market is that regional instability does not necessarily translate into an entirely negative outcome. When concerns about security and asset preservation rise in surrounding regions, corporations and high-net-worth individuals are more likely to seek refuge for their residences, offices, and assets in Dubai.

In the past, there have been periods where capital inflows into Dubai intensified after external shocks. This time too, if the conflict remains limited and the UAE's urban functions and international image of safety are maintained, a scenario where demand returns after a short wait-and-see period is entirely plausible.

Of course, if the conflict protracts or its scope expands, the outlook will change. In that case, the decline in transaction volumes could be prolonged, and sentiment-driven price adjustments might extend to a wider range. However, even in such a scenario, the key question is likely 'when will it recover,' rather than 'will the market be permanently destroyed'.

Summary

It is natural for the Dubai real estate market to experience short-term tension in the wake of a potential Iran conflict. However, looking back at past crisis periods, the Dubai market has consistently recovered through institutional improvements and a return of demand, even after experiencing temporary stagnation with each external shock.

The baseline scenario at present is short-term stagnation, not a complete collapse. What should be watched going forward, more than the news headlines themselves, are the speed of transaction volume recovery, the presence or absence of capital inflows, and price reactions across different segments. Instead of uniformly pessimistic views on the entire market, a calm assessment based on past examples and current market structure is what is most crucial now.